In today’s fast-paced world, setting financial goals has become increasingly important. Whether it’s saving for a down payment on a house, paying off debts, or starting a business, having a clear target gives us purpose and direction. However, the path to achieving these goals is often paved with financial challenges and obstacles. That’s where intelligent saving strategies come into play. By adopting effective methods and techniques, you can make progress toward your goals and build a solid financial foundation for the future.

Assess Your Current Financial Situation

The first step in any successful savings plan is evaluating your current financial situation. Take a deep dive into your income, expenses, and debts. Review your monthly budget and identify areas where you can cut back and save. This could involve reducing unnecessary expenses like dining out or subscriptions, negotiating better deals on bills, or finding alternatives for costly services. By understanding your financial standing, you can plan accordingly and make informed choices.

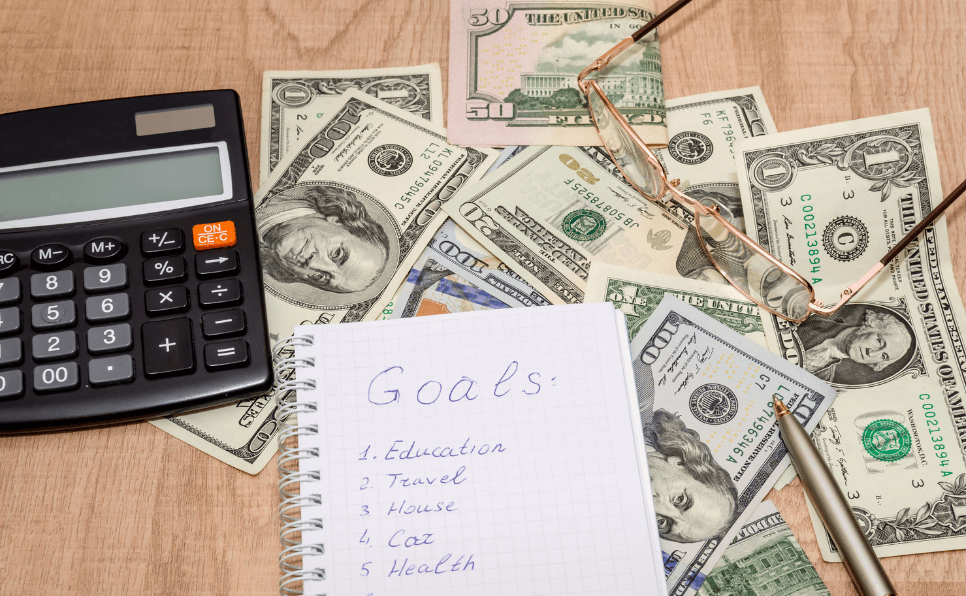

Define Your Specific Financial Goal

To effectively save, you need a specific target in mind. Please identify what you are saving for, whether it’s a short-term or long-term goal. Be as precise as possible, such as saving $10,000 for a down payment on a home or paying off $5,000 of credit card debt within six months. Setting a realistic and measurable goal helps you stay focused and motivated throughout the saving journey.

Create a Budget That Supports Your Goal

Budgeting is a powerful tool that can help you allocate your funds toward achieving your financial goal. Identify the amount you need to save each month and prioritize it within your budget. Cut back on non-essential expenses, redirecting that money towards your savings. Keep in mind that this does not mean sacrificing all enjoyment but rather finding a balance between saving and spending.

Create a Budget That Supports Your Goal

One of the easiest ways to ensure consistent savings is to automate the process. Set up automatic transfers from your checking account to a separate savings account. This can be done on a monthly or bi-weekly basis, aligning with your pay schedule. By automating your savings, you remove the temptation to spend the money elsewhere and make saving a priority.

Reduce Discretionary Spending

Another effective strategy for saving is reducing discretionary spending. Take a close look at your discretionary expenses, such as entertainment, shopping, or eating out. Identify areas where you can cut back without significantly impacting your quality of life. Implement strategies like mindful spending, where you pause and consider if an expense is essential, and delayed gratification, where you prioritize saving over instant gratification.

Explore Ways to Increase Income

To supercharge your savings, consider exploring ways to increase your income. This may involve taking on a side hustle, freelancing, or finding part-time work. Alternatively, you can monetize your hobbies or skills by offering services or creating products. The additional income can be directly channeled towards your financial goal, accelerating your saving progress.

Minimize Debt and Interest Payments

High-interest debts can hinder your ability to save effectively. Prioritize paying off debts with high-interest rates first, as they accumulate additional costs over time. Consider consolidating debts or negotiating lower interest rates to ease the burden and free up more money for savings. By reducing your debt load, you’ll have more room in your budget for saving.

Track Your Progress and Make Adjustments

Regularly tracking your saving progress is essential to stay on track. Keep a close eye on your savings account balance and gauge how well you are progressing towards your goal. If you notice any discrepancies or difficulties, be open to making adjustments to your strategy. This flexibility ensures that your saving plan remains realistic and achievable.

Stay Motivated and Celebrate Milestones

Saving towards a specific financial goal can sometimes feel like a never-ending journey. To stay motivated, acknowledge and celebrate milestones along the way. Whether it’s reaching a set savings amount or successfully paying off a debt, recognize your progress and reward yourself. Additionally, seek support from friends and family who can provide encouragement and accountability.

Striving to achieve financial goals requires dedication, discipline, and smart saving strategies. By assessing your current situation, defining your goals, creating a budget, automating savings, reducing discretionary spending, increasing income, minimizing debts, and tracking progress, you can make significant headway toward your financial aspirations. Remember to stay motivated and celebrate milestones, as this will help you maintain your focus and commitment. With perseverance and adaptability, you can turn your dreams into reality and build a secure financial future.

{kind=link}